2023 Outlook

The current bear market began roughly the same time the ball in Time Square dropped to usher in 2022,

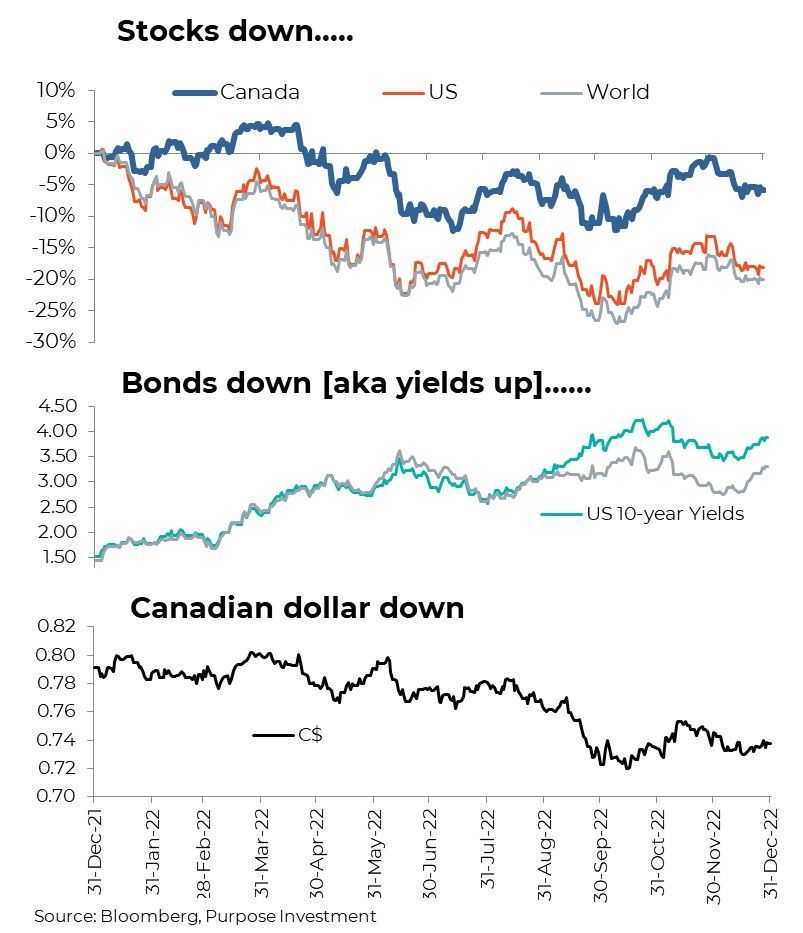

which means with the more recent ball drop this bear celebrated its one-year anniversary. There is no blueprint for bear markets. Sometimes they are short (2020), sometime long (2000-03). The magnitude of the price changes can vary and have certainly had a varied impact across different equity markets this go around. Global equities dropped by -18% in 2022 (in USD), same as the S&P 500 while the tech heavy NASDAQ dropped -33%. But Europe was down only -9%, Japan down -7% and Canada at -6% was one of the better performing markets. Sometimes bear markets are accompanied by a global recession, sometimes not.

Despite the variations and with inflation as the likely initial trigger of this bear making it rather unique, it is roughly following a normal bear market progression.

There is likely more to go in this bear market process which could even manifest as the market’s biggest fear migrates from inflation to recession. There is good news too. Equity valuations have come considerably and, in many pockets, may already be pricing in a recession. This provides a buffer in case there is more bad news ahead. And bond valuations, aka yields, are now attractive. There is also the forward-looking aspect of the equity markets. Often bottoming quarters ahead of the economic trough and even bottoming before the earnings trough.

This is a synopsis of our outlook thoughts heading into 2023 as we don’t get paid to sit on the fence: 2023 should start off decently as inflation comes down a bit more partially alleviating the markets biggest fear. Plus a little January effect could certainly help. However, less inflation will start to accelerate slowing corporate earnings. And the wealth effect of falling equity/bond markets over the past year plus delayed economic impact of rate hikes / higher yields will cause economic growth to fall significantly. This could trigger the final leg down of the bear and create the better buying opportunity, hopefully sometime in the 1st half, as the market begins to look through the trough and rally back to be positive on the year.

Of course the only recurring theme with investing more persistent than cycles, is markets surprise us all in the end. Below we have provided a recap of 2022 plus a few potential surprises ahead.

Market Recap – 2022 the great reset 2023 Market Surprises

The global economy downshifted substantially, from a 5.8% growth pace in 2021 (that is really high) to a more subdued 3.0% in 2022 (current estimates given the final quarterly data is still pending). 3.0% isn’t bad but the size of the drop from the previous year certainly made it more noticeable. With inflation and a still expanding economy, bond yields marched higher in 2022, creating a tough year for bonds. Equities were also hit, but not evenly. European markets were weighed down by what is likely a recession in the region, Asian markets by China’s zero covid policy plus a real estate popping. The U.S. market was a tail of two markets as growth stocks were crushed and value stocks held in much better (S&P 500 Growth -29%, S&P 500 Value 5% YTD). The TSX was a star, if a star can be one that is simply down much less. The Canadian market benefited from being very valued tilted and not much exposure to the growth tech space. And of course having companies involved in energy & food was a plus given supply disruptions caused by the war in Ukraine.

Despite the variations and with inflation as the likely initial trigger of this bear making it rather unique, it is roughly following a normal bear market progression.

- Speculative end game for the bull: The market become highly speculative in a number of areas, with lots of talk ‘it is different this time’. Maybe this time it was more ‘you are just too old to understand __________’. The blank could be crypto, Gamestop/Meme stocks, disruptive technologies, take your pick.

- Speculative areas get hit: This started in late 2021 as many of the areas in the markets that enjoyed outsized returns over the previous years, popped.

- Bear begins: As 2022 started, the price declines spread from the speculative pockets to the rest of the market. We can blame inflation, central banks, yields or the war. Nonetheless, prices of things in bear markets come down. That is what we experienced in 2022, not a straight line of course as the path had many twists and turns.

- Earnings: Up until recently corporate earnings held up really well, in part thanks to the ‘getting back to normal’ behaviours and inflation (remember earnings are nominal so inflation often helps earnings). But as 2023, earnings growth is slowing, revisions are negative. Earnings contraction is normal in bears and this phase may be starting to get going.

- Recession: The economy often seems like it doesn’t react much, and then it moves quickly. Global economic activity has been slowing, and some countries are likely in a recession today, but others remain decently healthy. What lies ahead is something between a slow down, a shallow recession or a recession. With strong arguments and data supporting all three.

- Capitulation: Many have opined that an investor capitulation remains a missing ingredient to mark the potential end of the bear. This could be in store for 2023, or maybe it doesn’t happen this go around.

There is likely more to go in this bear market process which could even manifest as the market’s biggest fear migrates from inflation to recession. There is good news too. Equity valuations have come considerably and, in many pockets, may already be pricing in a recession. This provides a buffer in case there is more bad news ahead. And bond valuations, aka yields, are now attractive. There is also the forward-looking aspect of the equity markets. Often bottoming quarters ahead of the economic trough and even bottoming before the earnings trough.

This is a synopsis of our outlook thoughts heading into 2023 as we don’t get paid to sit on the fence: 2023 should start off decently as inflation comes down a bit more partially alleviating the markets biggest fear. Plus a little January effect could certainly help. However, less inflation will start to accelerate slowing corporate earnings. And the wealth effect of falling equity/bond markets over the past year plus delayed economic impact of rate hikes / higher yields will cause economic growth to fall significantly. This could trigger the final leg down of the bear and create the better buying opportunity, hopefully sometime in the 1st half, as the market begins to look through the trough and rally back to be positive on the year.

Of course the only recurring theme with investing more persistent than cycles, is markets surprise us all in the end. Below we have provided a recap of 2022 plus a few potential surprises ahead.

Market Recap – 2022 the great reset 2023 Market Surprises

- Inflation cooling carries a grey cloud

- Recession: none, soft or hard

- Value & Dividends

- Simplified yield

- International diversification back in vogue

2022 – The Great Reset

How do we even attempt to unpack what happened in 2022, on the surface very little sounds good. Russia invaded Ukraine, a travesty, that also caused increased global political polarization, an energy crisis and higher food prices. Global inflation got out of control, not from the war but more from the knock-on effects of the pandemic altered behaviours. Plus the impact of global monetary/fiscal stimulus that was left on too long. Inflation triggered an abrupt reversal in stimulus from accommodation to restriction as just about all central banks tightened financial conditions, some materially.The global economy downshifted substantially, from a 5.8% growth pace in 2021 (that is really high) to a more subdued 3.0% in 2022 (current estimates given the final quarterly data is still pending). 3.0% isn’t bad but the size of the drop from the previous year certainly made it more noticeable. With inflation and a still expanding economy, bond yields marched higher in 2022, creating a tough year for bonds. Equities were also hit, but not evenly. European markets were weighed down by what is likely a recession in the region, Asian markets by China’s zero covid policy plus a real estate popping. The U.S. market was a tail of two markets as growth stocks were crushed and value stocks held in much better (S&P 500 Growth -29%, S&P 500 Value 5% YTD). The TSX was a star, if a star can be one that is simply down much less. The Canadian market benefited from being very valued tilted and not much exposure to the growth tech space. And of course having companies involved in energy & food was a plus given supply disruptions caused by the war in Ukraine.

Simply put, 2022 was not a kind year for investors. Just look at the traditional 60/40 portfolio, let’s say 20% TSX, 20% US, 20% international and 40% Canadian bonds. Thanks to a falling Canadian dollar which helped buffer the drop in non-Canadian investments, this portfolio would be down about 10% on the year. Worse yet, the bonds, which typically play the role of portfolio stabilizer were responsible for almost half the decline.

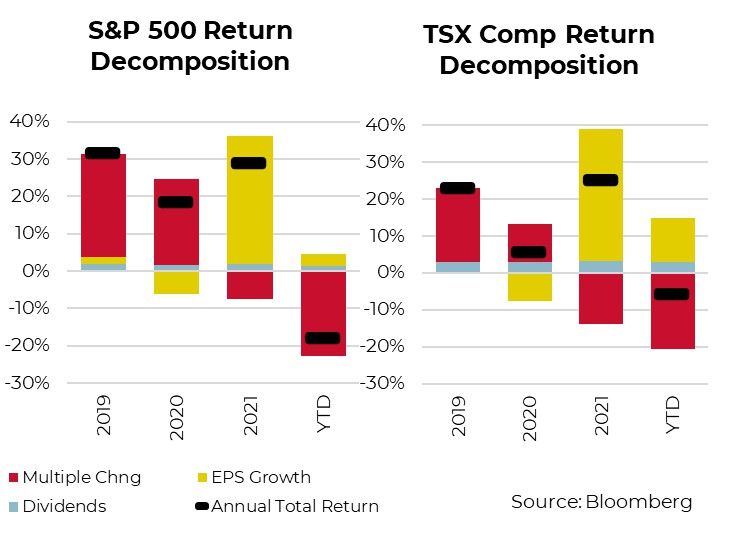

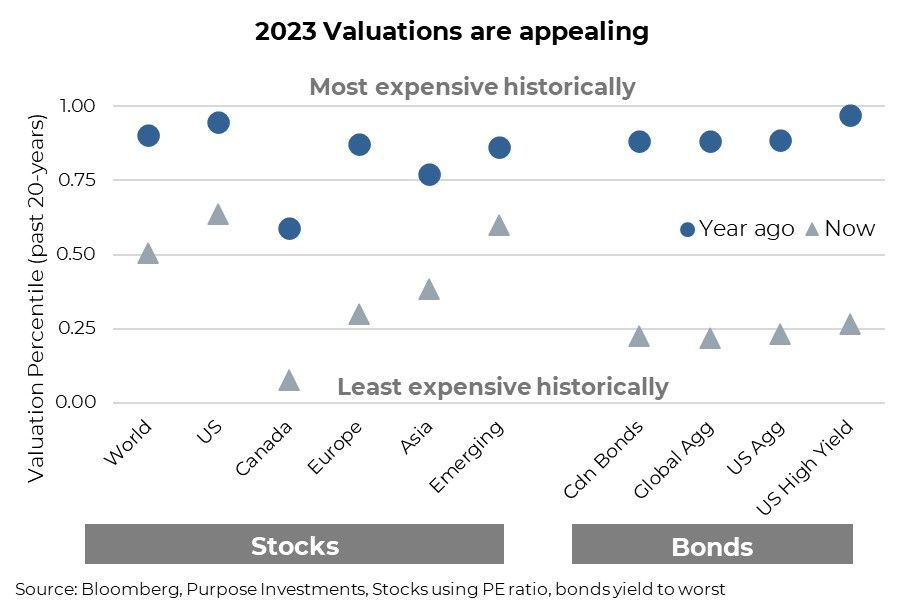

The silver lining is 2022 appears to have reset markets. Now we are not saying the reset is over, or the bottom of the bear is in, or even that bond yields are done going up, but things are much more balanced now. Bonds actually carry an attractive yield now after not doing so for many years. And equities, while not cheap and perhaps earnings estimates will

continue to fall, are not expensive. Note the red bars in the return decompositions for the S&P 500 and TSX in the YTD (year-to-date) column. The valuation multiples have contracted substantially.

The valuations for bonds and equities went from expensive at the start of the year to cheap or at least fairly valued by the end. Mainly because we moved from a world with excess liquidity that was very cheap to a world with less liquidity and the cost of capital matters again. A painful journey, no doubt, but one that begins to plant the seeds of the next cycle.

Inflation cooling carries a grey cloud Last year, the biggest issue for markets quickly became inflation, in case you missed the evening news that kept the price of bananas front and center. CPI, the most common measure, reached high single digits in many countries including the U.S. and Canada, highest levels in decades. Pandemic changed behaviours, supply issues, too much money, the list of causes is widely known and talked about. And while we believe inflation will remain a more recurring market topic in the years ahead, in 2023 its path should continue to be in the cooling direction. The pandemic influenced behaviours are getting much closer to normal, the money is being sucked out of the system and the economy is slowing.

Inflation is unlikely to get back to pre-pandemic stable levels, that was the last cycle. But it should continue to grind down from currently levels during 2023 and as it does the market will pay less and less attention [ok, the market doesn’t pay attention but the reaction to the data should become more muted]. This should slow and then stop the continuous rate hikes that we all weathered in 2022.

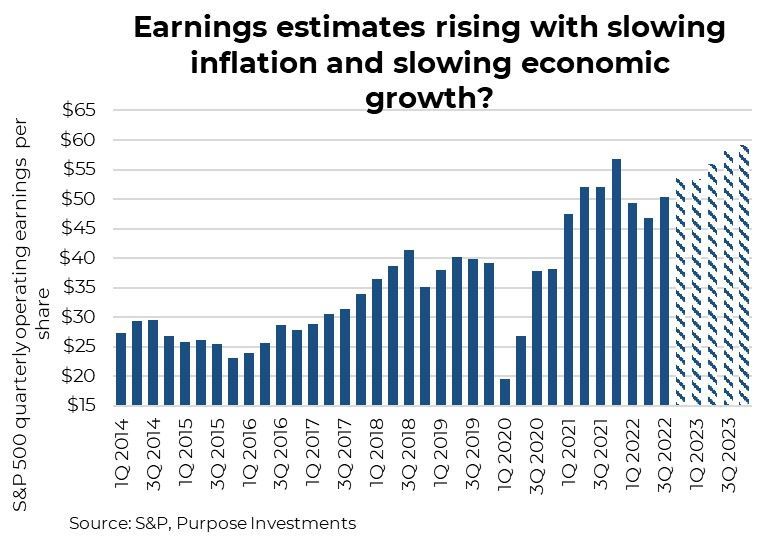

This is good news and if the inflation data continues to cool, markets can rally around this. Talk of a Fed pivot or arresting rate hikes would be a big positive. But, cooling inflation plus slowing economic activity are a bad combination for corporate earnings. The market is already starting to price in a little bit of slowing earnings growth based on consensus estimates, so this isn’t a surprise. The question will be the degree or magnitude.

The valuations for bonds and equities went from expensive at the start of the year to cheap or at least fairly valued by the end. Mainly because we moved from a world with excess liquidity that was very cheap to a world with less liquidity and the cost of capital matters again. A painful journey, no doubt, but one that begins to plant the seeds of the next cycle.

2023 Market Surprises

Last year was one of surprises, most of which were not market friendly. Now comes the hard part, what could the surprises of 2023 hold for investors? And what does it all mean for portfolio construction. Below we highlight a number of important themes for 2023 and our take on them from an investor perspective. But if history is any guide, there will be surprises…..Inflation cooling carries a grey cloud Last year, the biggest issue for markets quickly became inflation, in case you missed the evening news that kept the price of bananas front and center. CPI, the most common measure, reached high single digits in many countries including the U.S. and Canada, highest levels in decades. Pandemic changed behaviours, supply issues, too much money, the list of causes is widely known and talked about. And while we believe inflation will remain a more recurring market topic in the years ahead, in 2023 its path should continue to be in the cooling direction. The pandemic influenced behaviours are getting much closer to normal, the money is being sucked out of the system and the economy is slowing.

Inflation is unlikely to get back to pre-pandemic stable levels, that was the last cycle. But it should continue to grind down from currently levels during 2023 and as it does the market will pay less and less attention [ok, the market doesn’t pay attention but the reaction to the data should become more muted]. This should slow and then stop the continuous rate hikes that we all weathered in 2022.

This is good news and if the inflation data continues to cool, markets can rally around this. Talk of a Fed pivot or arresting rate hikes would be a big positive. But, cooling inflation plus slowing economic activity are a bad combination for corporate earnings. The market is already starting to price in a little bit of slowing earnings growth based on consensus estimates, so this isn’t a surprise. The question will be the degree or magnitude.

The shaded bars have not yet been reported and are based on consensus forecasts. Margins are at historical highs with costs rising, so unlikely to see margins improve. The U.S. dollar has been strong, another headwind for earnings. Add slowing inflation and slowing economic growth, forecasts are still way too high.

Oh, and one more thing. A good portion of earnings growth in the past decade came from share buybacks, much of which was debt financed. The old strategy of issuing debt (remember when yields were really low) and using proceeds to buy back shares, this activity manufactured earnings growth. Now with less liquidity in the bond market and the cost of debt materially higher, this strategy is caput. And general financing costs are now higher, another drag.

The potential earnings recession will disproportionately impact some and not others. Companies able to pass on higher prices will be at an advantage. As will those with less cost pressures. Interest costs and the balance sheet is quickly becoming a performance determinant again. Yes, financial analysis may be back in vouge.

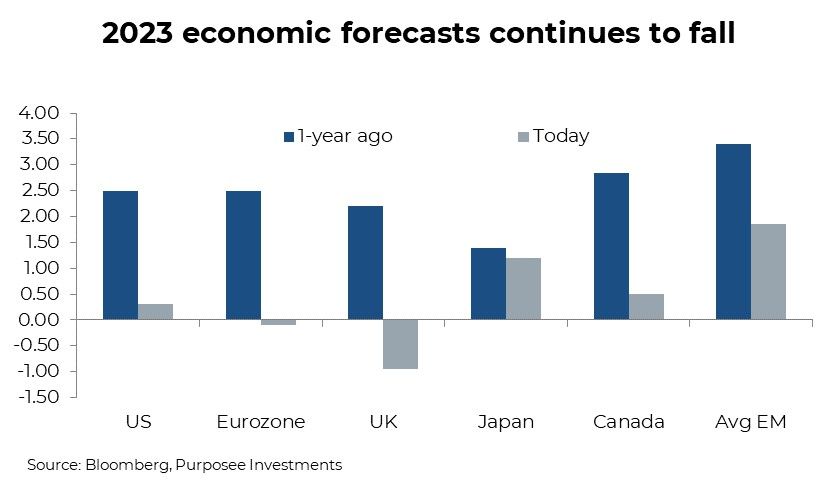

Recession: none, soft or hard There is no denying economic activity is slowing but so far the market has not cared much as it has taken a backseat to inflation angst. Slowing economic activity has also been masked by decent labour markets as service jobs are still being replenished from the pandemic induced capacity reductions. This is still one weird economy being influenced by the reverberations from the pandemic. 2023 economic forecasts for the U.S. have evaporated to nearly zero, same with Canada. The Eurozone and UK have seen their prospects for 2023 turn negative.

Oh, and one more thing. A good portion of earnings growth in the past decade came from share buybacks, much of which was debt financed. The old strategy of issuing debt (remember when yields were really low) and using proceeds to buy back shares, this activity manufactured earnings growth. Now with less liquidity in the bond market and the cost of debt materially higher, this strategy is caput. And general financing costs are now higher, another drag.

The potential earnings recession will disproportionately impact some and not others. Companies able to pass on higher prices will be at an advantage. As will those with less cost pressures. Interest costs and the balance sheet is quickly becoming a performance determinant again. Yes, financial analysis may be back in vouge.

Recession: none, soft or hard There is no denying economic activity is slowing but so far the market has not cared much as it has taken a backseat to inflation angst. Slowing economic activity has also been masked by decent labour markets as service jobs are still being replenished from the pandemic induced capacity reductions. This is still one weird economy being influenced by the reverberations from the pandemic. 2023 economic forecasts for the U.S. have evaporated to nearly zero, same with Canada. The Eurozone and UK have seen their prospects for 2023 turn negative.

It has been our experience when the consensus economists change forecasts to this degree, they are trying to catch up with reality. In other words, those lowered estimates are probably still too optimistic. This raises the question: Recession, shallow recession or no recession at all? Here are our thoughts, some are positive and some negative:

+ Healthy Consumer - Much is talked about the health of the consumer. Not so much the Canadian one but the U.S. and European consumer has less debt and has saved over the pandemic years. Labour markets remain very healthy and wage growth is positive. + It was always going to look like a recession – The pandemic induced behaviours brought forward a lot of spending on durable goods at the expense of services. This helped super charge the global economy, since buying an iPad has a bigger economic impact than buying a pint of beer. As we ‘society’ came off this ‘goods’ buying high, and re-allocated to services, it was bound to manifest in a slowdown. + Desynchronized economic activity – In 2008 and 2020, all economies went over the cliff at the same time. One was credit driven the other a pandemic. Today, economic growth is much more desynchronized. China slowed a lot in 2022 and may now be starting to improve as covid policy is changed plus some encouraging real estate signs. Europe is likely in a recession now given inflation and energy hit. Canada may be in one in 2023 with our overly sensitive economy to housing. Perhaps the US slows afterwards. But others may be on the mend by then. This desynchronized activity is good as it lessens the blow to markets. + Xi pivot – There is much talk of a potential Fed pivot in 2023, which we really don’t see occurring unless something goes terribly wrong in the economy or markets. Fed pause is likely the best scenario. China on the other hand has been experiencing a continued economic slowdown due to a real estate crisis (of sorts) and the zero covid policy. On a positive it appears the zero covid policy is being steadily dismantled. The path is still unknown but economically speaking this is good news. And there are some signs the real estate pain may be starting to ease. - Rate hikes / yields – It always seems the economy is really slow to react….and then it suddenly does react. Higher interest rates impact consumers, business spending and the cost of capital. While it is debatable how long the lag is between changes in rates and when it is felt in the economy, but if its 9-months then only 1 of the 7 Fed rate hikes has been felt so far. Oh, and that one was the small 25bps variety. The economy is about to really start to feel the rest. - Wealth effect – The global bear market in equities and bonds has reduced total wealth by $139 trillion. That is $25 trillion from equities and $114 trillion from the global bond market. These global market capitalization measures are in US dollars, so let’s adjust for the rising USD and the damage is more reasonable at about $65 trillion (rough calculations now, fortunately when talking trillions it doesn’t have to be exact). But, global inflation last year based on the World Economy Weighted inflation index was 9.7%. Which means the world’s wealth, ignoring the market price performance, became almost 10% less valuable. Add that back in and we are about back to the $139 trillion in reduced real wealth. This drop will begin to weigh on the economic decisions of consumers and businesses.

+ Healthy Consumer - Much is talked about the health of the consumer. Not so much the Canadian one but the U.S. and European consumer has less debt and has saved over the pandemic years. Labour markets remain very healthy and wage growth is positive. + It was always going to look like a recession – The pandemic induced behaviours brought forward a lot of spending on durable goods at the expense of services. This helped super charge the global economy, since buying an iPad has a bigger economic impact than buying a pint of beer. As we ‘society’ came off this ‘goods’ buying high, and re-allocated to services, it was bound to manifest in a slowdown. + Desynchronized economic activity – In 2008 and 2020, all economies went over the cliff at the same time. One was credit driven the other a pandemic. Today, economic growth is much more desynchronized. China slowed a lot in 2022 and may now be starting to improve as covid policy is changed plus some encouraging real estate signs. Europe is likely in a recession now given inflation and energy hit. Canada may be in one in 2023 with our overly sensitive economy to housing. Perhaps the US slows afterwards. But others may be on the mend by then. This desynchronized activity is good as it lessens the blow to markets. + Xi pivot – There is much talk of a potential Fed pivot in 2023, which we really don’t see occurring unless something goes terribly wrong in the economy or markets. Fed pause is likely the best scenario. China on the other hand has been experiencing a continued economic slowdown due to a real estate crisis (of sorts) and the zero covid policy. On a positive it appears the zero covid policy is being steadily dismantled. The path is still unknown but economically speaking this is good news. And there are some signs the real estate pain may be starting to ease. - Rate hikes / yields – It always seems the economy is really slow to react….and then it suddenly does react. Higher interest rates impact consumers, business spending and the cost of capital. While it is debatable how long the lag is between changes in rates and when it is felt in the economy, but if its 9-months then only 1 of the 7 Fed rate hikes has been felt so far. Oh, and that one was the small 25bps variety. The economy is about to really start to feel the rest. - Wealth effect – The global bear market in equities and bonds has reduced total wealth by $139 trillion. That is $25 trillion from equities and $114 trillion from the global bond market. These global market capitalization measures are in US dollars, so let’s adjust for the rising USD and the damage is more reasonable at about $65 trillion (rough calculations now, fortunately when talking trillions it doesn’t have to be exact). But, global inflation last year based on the World Economy Weighted inflation index was 9.7%. Which means the world’s wealth, ignoring the market price performance, became almost 10% less valuable. Add that back in and we are about back to the $139 trillion in reduced real wealth. This drop will begin to weigh on the economic decisions of consumers and businesses.

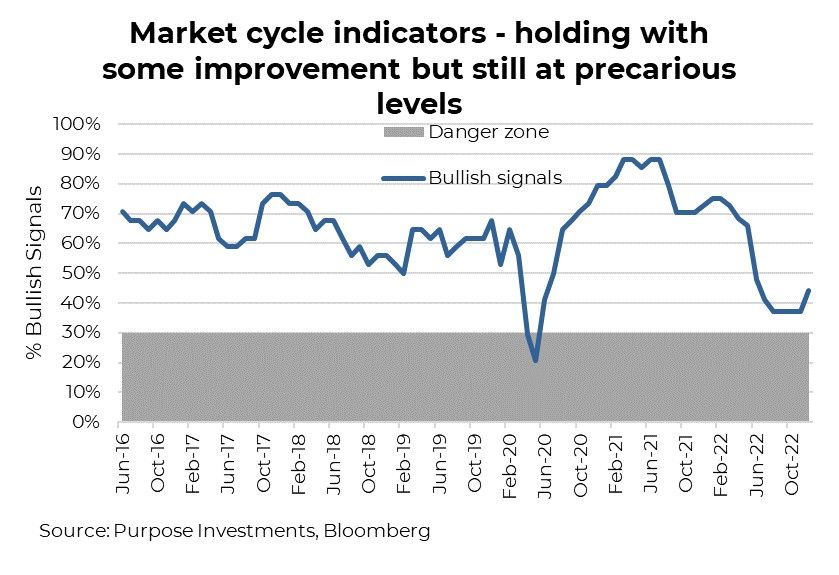

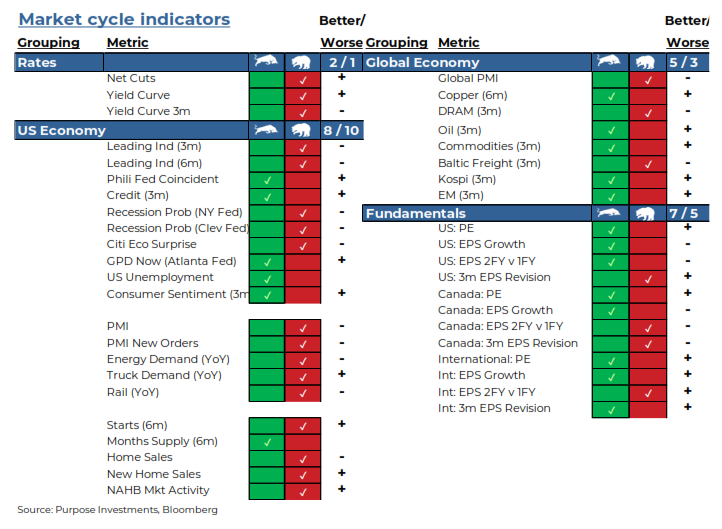

Add it all up and the only thing clear is it is not clear. This is also captured in our Market Cycle framework which continues to sit just above the danger zone that typically is associated with a recession.

We believe there is a more material economic slowdown ahead in 2023 which the market may begin to pay more attention.

2023 Portfolio Construction

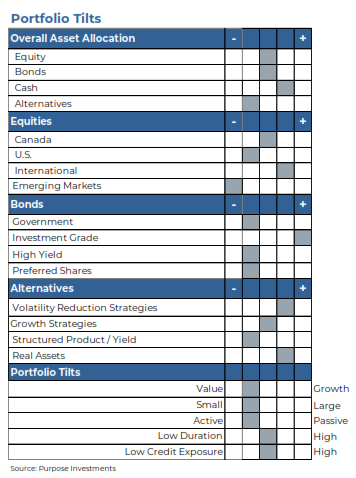

We have no abrupt changes to our portfolio allocations to start the year. Our optimism on improved pricing in many areas of the market is tempered by the near term path ahead. This has us hugging the neutral line in many categories such as equity and bond allocations. Little extra cash poised to be deployed should more weakness develop. And a mild underweight in alternatives given how far along this bear market has become and the ability to now find defense in traditional bonds.With a value and small tilt among equities, we remain more sanguine for the U.S. market, neutral on Canada and bit of an overweight international. China’s pivot is positive for emerging markets but given tightening financial conditions we are not.

Our bond weighting is neutral and we have increased duration during the year to a more neutral stance. For a balanced profile this is about 4.5 to 5. Yields may rise further but at current levels the risk/return is more balanced considering there may be a recession of sorts on the horizon. There is no denying that valuations are much more attractive as we head into 2023. Perhaps equity earnings are not as solid as we would like but many markets appear to be pricing a decent amount of bad news ahead. And bonds too offer some of the better yields of the past two decades. Valuations, for either bonds or equities, are in a much better place than at the start last year.

Portfolio thoughts heading into 2023

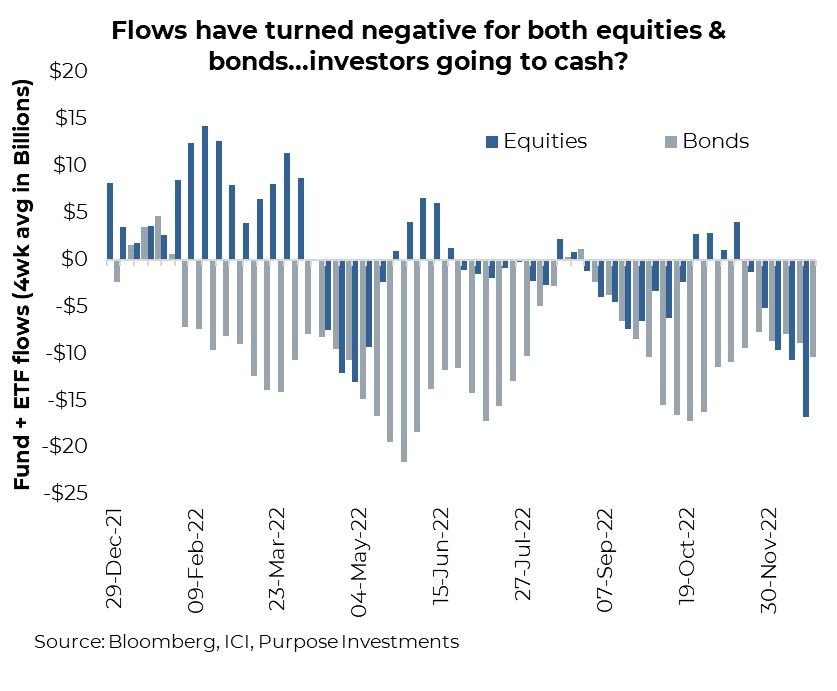

There may be some added optimism if you look at fund & ETF flows during 2022, especially near the end. Not too surprising bond outflows were pretty sizeable and persistent as yields moved higher (prices lower). Interesting that anecdotal information seems to indicate institutions are now more active in increasing their traditional bond allocations. Equity flows are even more interesting and capture investor behaviour. During the early part of this bear market, the ‘buy the dippers’ were active (positive blue bars in early ’22). As the bear dragged on, this behaviour ended as optimism this was just a short period of market weakness faded. But investor held on and remained invested. Until late 2022 when we have started to see increased outflows and increased inflows to cash.

If this trend continues or accelerates, it may just be the start of the capitulation event this bear market has been missing. Or it was just some more aggressive tax loss selling. Either way, the flows into cash and lack of investor appetite is encouraging that the end of the bear may be getting closer.

Below we have highlighted a few ideas for portfolio allocations:

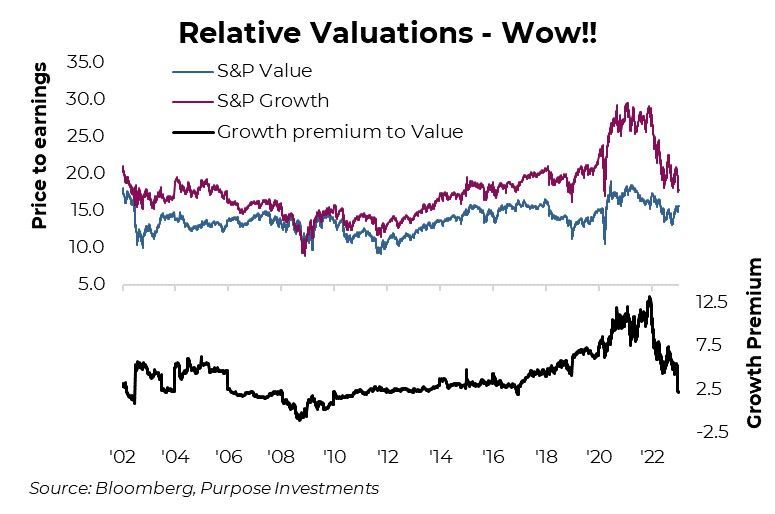

Value & Dividends The growth factor has so far taken the brunt of this bear market, just look at the relative performance of the S&P 500 Growth Index (-29%) and S&P 500 Value Index (-5%) in 2022. This has help alleviate the valuation premium of growth that had reached nosebleed levels in 2021. And there are some factors that support the growth factor heading into 2023. A mere 2 point valuation premium is appealing. Inflation is set to cool in the coming months which is a positive for growth given its longer duration characteristics. And overall earnings growth is slowing, another positive for growth.

Below we have highlighted a few ideas for portfolio allocations:

Value & Dividends The growth factor has so far taken the brunt of this bear market, just look at the relative performance of the S&P 500 Growth Index (-29%) and S&P 500 Value Index (-5%) in 2022. This has help alleviate the valuation premium of growth that had reached nosebleed levels in 2021. And there are some factors that support the growth factor heading into 2023. A mere 2 point valuation premium is appealing. Inflation is set to cool in the coming months which is a positive for growth given its longer duration characteristics. And overall earnings growth is slowing, another positive for growth.

This may set the stage for a relief rally in the growth factor over value. However, as 2023 grinds on and a newcycle begins, we believe Value will be the winning factor. For one leadership change is afoot and while the new leaders remain unknown, we have a good deal of confidence it won’t be the previous leaders which are more dominant in the growth factor. In fact, the last leaders still represent a high weighting in the indices which may become a headwind for some cap weighted indices.

We also expect nominal economic growth (GDP + inflation) to be higher in the coming cycle compared to the last. This should favour the value factor over growth. And yields to remain at higher levels this cycle with greater variability, also favouring value.

While the U.S. equity market has a well defined value and growth factor, it is a bit more complex in other markets. The TSX is a value market in general, notably with the dividend subset factor. International markets, given current valuations, would also mostly be viewed as heavy in the value factor. This is further supporting rationale for our current underweight U.S. (a growth heavy index), market weight in Canada and overweight in international equities.

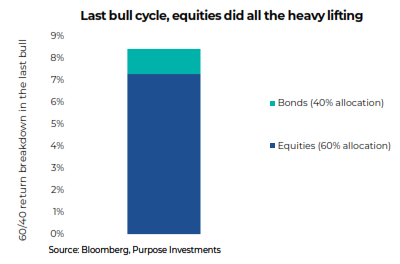

We are not contending that any of these measures are cheap; that will depend on their valuation or yield a few years down the road. But we can say after the painful reset in 2022, when everything simply fell in value, the market is much more balanced or fair today. This should better balance out returns in the next cycle. There is no denying returns in the last bull came mainly from the equity side of the portfolio. The following chart is the return attribution for a 60/40 portfolio from the end of 2009 to the end of 2021 (before this bear). With total performance a little over 8% annualized, almost all the performance came from equities.

As we near the start of the next bull, it would appear that yield is now plentiful. Available in equities, bonds and cash. Given the biggest contributor to bond returns are the yield at the time of purchase, these higher bond yields should better balance the performance contribution for portfolios. This bond & equity bear of 2022 may have actually reset returns in favour of the old boring 60/40. It’s been a painful journey to get here, but it’s a much more balanced investment landscape.

We also expect nominal economic growth (GDP + inflation) to be higher in the coming cycle compared to the last. This should favour the value factor over growth. And yields to remain at higher levels this cycle with greater variability, also favouring value.

While the U.S. equity market has a well defined value and growth factor, it is a bit more complex in other markets. The TSX is a value market in general, notably with the dividend subset factor. International markets, given current valuations, would also mostly be viewed as heavy in the value factor. This is further supporting rationale for our current underweight U.S. (a growth heavy index), market weight in Canada and overweight in international equities.

Simplified yield

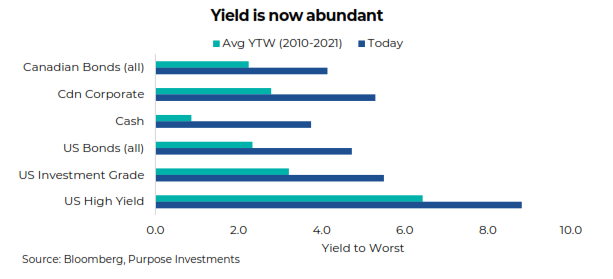

This bear market may not be over yet, and yields could tick higher, equities lower, earnings could fall, and maybe even a recession. But already, there has been a massive reset of valuations and expectations. The speculative fever that was evident late in the last cycle is clearly gone, just ask any venture capitalist trying to raise money. Today, you can buy the TSX with a dividend yield of 3.3% and trading at a valuation of 12x. The Canadian bond universe now yields 4.2%, while the corporate subset yields 5.4%. The majority of bonds now trade below par, and cash has a decent return.We are not contending that any of these measures are cheap; that will depend on their valuation or yield a few years down the road. But we can say after the painful reset in 2022, when everything simply fell in value, the market is much more balanced or fair today. This should better balance out returns in the next cycle. There is no denying returns in the last bull came mainly from the equity side of the portfolio. The following chart is the return attribution for a 60/40 portfolio from the end of 2009 to the end of 2021 (before this bear). With total performance a little over 8% annualized, almost all the performance came from equities.

As we near the start of the next bull, it would appear that yield is now plentiful. Available in equities, bonds and cash. Given the biggest contributor to bond returns are the yield at the time of purchase, these higher bond yields should better balance the performance contribution for portfolios. This bond & equity bear of 2022 may have actually reset returns in favour of the old boring 60/40. It’s been a painful journey to get here, but it’s a much more balanced investment landscape.

Simplify your income – In the last cycle, with yields so low and generally trending lower during the cycle, the stretch to find yield really had to get creative to meet investor demand. Very successful strategies were created to find yield in faraway locations, create yield with more exotic trading strategies, or gain access to yielding assets previously unavailable. Many proved very successful and certainly helped fill a demand caused by this low-yield environment.

Today with yield now being abundant, does your portfolio need to be as creative? Many of the strategies developed and used today carry other risks, perhaps geographic or execution or some nuanced risk that few investors are aware. They may still have a place in a portfolio, but with plain vanilla yield now readily available, simplifying a portfolio’s yield component may prove prudent.

Today with yield now being abundant, does your portfolio need to be as creative? Many of the strategies developed and used today carry other risks, perhaps geographic or execution or some nuanced risk that few investors are aware. They may still have a place in a portfolio, but with plain vanilla yield now readily available, simplifying a portfolio’s yield component may prove prudent.

International Diversification Back In Vogue

It isn’t this simple, but it just might be. In the ‘80s, the U.S. sucked, as did the U.S. dollar (USD); meanwhile, international markets rocked. In the ‘90s, the U.S. rocked, as did the USD, while all other markets trailed. In the aughts, the U.S. lagged, plus a weak USD, while TSX and emerging markets (E.M.) crushed it. In the most recent bull, the ‘10s, the U.S. was the star again, plus a strong USD, while others lagged. If this simple long- term pattern follows, the ‘20s should be international/E.M. with weak U.S. and USD.

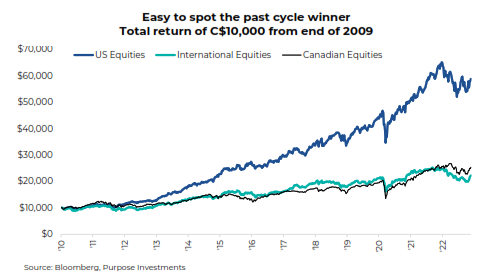

Geographic diversification has always been a core tenant of portfolio construction. Unfortunately, it’s been more like geographic ‘diworsification’ over the past cycle. A simple overweight U.S. equities has been the no-brainer portfolio allocation move, as seen in the chart. U.S. mega-cap tech has been the global cycle leader driving U.S. returns over the past cycle to outperform Canadian and international allocations significantly.

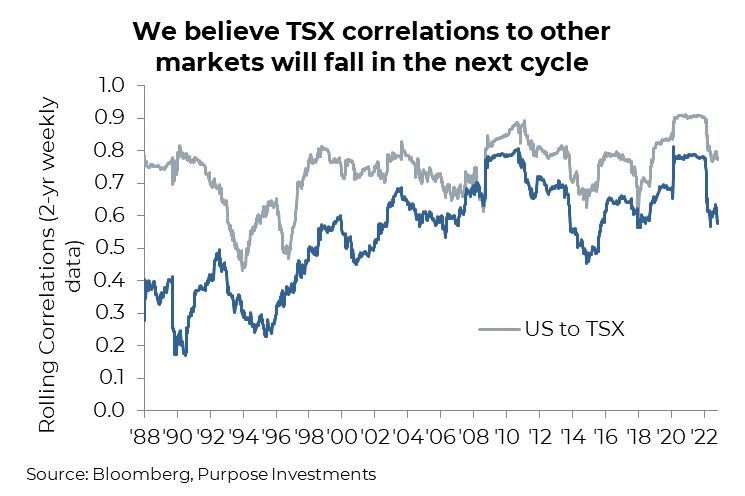

Besides the outright dominance of U.S. markets, the past cycle has been characterized by a sustained period of synchronized global growth, which has caused global correlations to rise, decreasing the benefits of international diversification. Higher correlations reduced the benefits of diversifying, but as the chart below shows, correlations have dropped from historically elevated levels. Correlations always get lower during bear markets, but it’s worth noting that international markets are still far less correlated to the TSX than the S&P 500. And if global growth is going to become less synchronized and more variable, the benefits of international diversification should continue to rise.

Besides the outright dominance of U.S. markets, the past cycle has been characterized by a sustained period of synchronized global growth, which has caused global correlations to rise, decreasing the benefits of international diversification. Higher correlations reduced the benefits of diversifying, but as the chart below shows, correlations have dropped from historically elevated levels. Correlations always get lower during bear markets, but it’s worth noting that international markets are still far less correlated to the TSX than the S&P 500. And if global growth is going to become less synchronized and more variable, the benefits of international diversification should continue to rise.

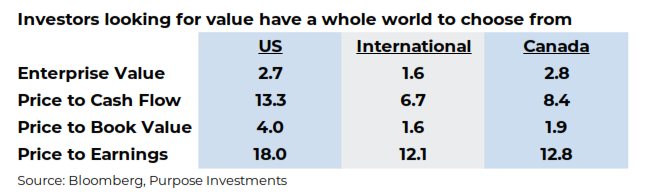

No single country can outperform all of the time. The global economy continues to evolve, and while we cannot predict the outcome of wars or policy decisions of foreign governments, we can quantify relative value. Global markets are considerably undervalued relative to U.S. equities across multiple measures. Given the depressed valuations, the likelihood of some degree of ‘catch-up’ during the next bull should suggest that international exposure can help investors experience a quicker recovery compared with less diversified portfolios.

Looking ahead through the next cycle, we expect to see a period of desynchronized global growth, which should only enhance the benefits of geographic diversification. Persistent pockets of inflation will likely decrease the degree of coordinated accommodative monetary policy around the globe leading to potentially large differences in country performance.

We published a lengthy report in December entitled ‘Preparing for the next bull’ to help investors and advisors to think about the next cycle. The report is long but so are bull markets, and positioning will count. Expect more instalments in this theme and of course if you would like to discuss in more detail, we are here to help.

Final note

We are constructive on portfolio returns in 2023. Yes, this bear may have more to grind asset prices lower but we do believe we are closer to the end (bottom) than the start. At some point this will usher in a new market cycle that will look and behave differently than the last bull cycle. The timing on when this will commence will only be known after the fact. But it is worth looking at portfolios and positioning, if it is still built for the last cycle, there may be some preparation to consider.We published a lengthy report in December entitled ‘Preparing for the next bull’ to help investors and advisors to think about the next cycle. The report is long but so are bull markets, and positioning will count. Expect more instalments in this theme and of course if you would like to discuss in more detail, we are here to help.

Copyright remains with Advisor Marketing for these articles, but it is not necessary to acknowledge copyright when using these articles. The content is your use only, to support and promote your individual practice. No exclusivity is granted with regards to these articles or their use.

— Craig Basinger is the Chief Market Strategist at Purpose Investments

— Brett Gustafson is a Portfolio Analyst at Purpose Investments

— Derek Benedet is a Portfolio Manager at Purpose Investments

Disclaimers

Echelon Wealth Partners Inc.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Echelon Wealth Partners Inc. or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Echelon Partners warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Echelon Wealth Partners Inc. is a member of the Investment Industry Regulatory Organization of Canada and the Canadian Investor Protection Fund.

Disclaimers

Echelon Wealth Partners Inc.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Echelon Wealth Partners Inc. or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Echelon Partners warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Echelon Wealth Partners Inc. is a member of the Investment Industry Regulatory Organization of Canada and the Canadian Investor Protection Fund.

Share this Blog

Inflation has been driving consumers and central bankers crazy over the past few years. As the numbers cool down we explore what this means going forward

When the stock market has a correction, we explore the best performing assets and if bonds have a place in today's investment portfolios

As recession fears lower we answer the question of if we are in a new cycle? This ain't that. We are still at the tail end of the previous cycle.

The markets are rising calmly with low volatility going into the summer that tends to be also low volatility

There are some weaker signals in the economy and that is exactly what the stock market is hoping for

With a valuation gap widening it might be a good time to revisit Emerging Markets

There is a lot of data that is pushing and pulling the markets right now. If you are looking for active management, ensure they are actually active

Corporate earnings have been coming in ahead of expectations in Q1. With the strong US dollar and stubborn interest rates it will be interesting to see if this trend persists in Q2.

Oil and gas companies, specifically the smaller ones, are where you can find value in today's market

There are reasons for the CAD to be weak against the USD but those reasons are diminishing